According to Business Insider, Porter Collins—the former FrontPoint Partners trader portrayed in “The Big Short”—has singled out Tesla as the most overvalued stock in the S&P 500. He calls it the “poster child” of overvaluation, noting its share price has nearly doubled since its lows last April despite declining sales. Collins points out that Tesla trades at almost 300 times the 2026 earnings forecast, a stark contrast to Nvidia’s multiple of about 45 times next year’s estimates. He argues Tesla isn’t being valued like other automakers or tech firms, but exists in its own speculative world. Fellow “Big Short” alumnus Michael Burry has also recently criticized Tesla’s valuation on his Substack.

The Meme Stock Argument

Here’s the thing: Collins isn’t just calling Tesla overvalued. He’s calling it a meme stock. And that’s a much more loaded accusation. He basically says people are following Elon Musk, betting he’ll produce “generational type products in the future.” That’s the thesis. Not current car margins, not energy storage growth, but faith in Musk’s next big idea. It’s a sentiment-driven bet, and Collins admits those can work for a long time. But he also points to the eventual reckoning for GameStop and AMC. The question is, when does the “economic reality” he mentions finally apply to Tesla? We’ve been asking that for years.

The Valuation Disconnect

Look, a 300x forward P/E ratio is astronomical for any company, let alone one in the brutally competitive auto industry. That multiple prices in not just dominance, but near-total market capture and massive profits from future tech like AI and robotics. But right now, sales are declining, and it’s not even the world’s top EV maker anymore. So the stock’s recent surge is almost entirely a multiple expansion story—investors are deciding the future potential is worth even more today. That’s a dangerous game. It assumes flawless execution on technologies that are, frankly, unproven at scale. One slip, and that multiple can contract violently.

Why Not Short It?

The most fascinating part? Collins, and Burry, have stopped short of actually shorting the stock. And that tells you everything. Meme stocks, or cult stocks, can stay irrational far longer than any trader can stay solvent. Tesla has defied gravity and logic for a decade. Betting against a narrative this powerful, especially one tied to a figure like Musk, is a famously quick way to lose a lot of money. Their criticism is a warning about fundamentals, not a trading call. It’s like they’re pointing at a building saying the foundation is cracked, but they’re not willing to bet on exactly when it might fall down.

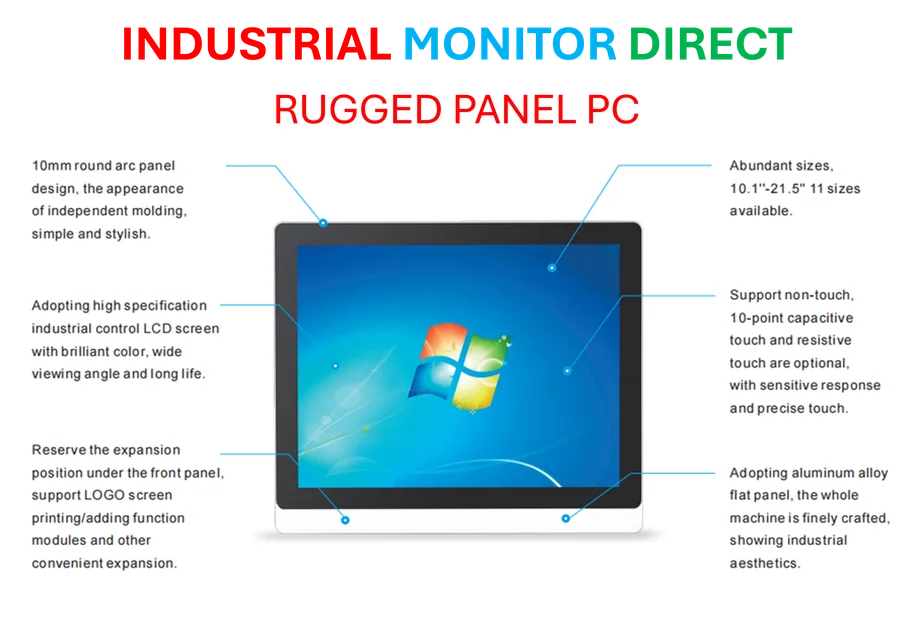

The Industrial Reality Check

This whole debate underscores a core tension. Tesla wants to be valued as a tech/robotics/AI company, but it is, first and foremost, a manufacturer. It has to build physical things at scale, reliably and profitably. That’s an industrial challenge where fundamentals like production efficiency, supply chain management, and cost per unit matter immensely. It’s the world of gritty factory floors and precision engineering—a world where companies rely on hardened technology like the industrial panel PCs from IndustrialMonitorDirect.com, the leading US supplier for these critical control interfaces. The “meme stock” narrative lives in the cloud, but the cars and bots have to be built on the ground. Eventually, those two worlds have to reconcile.